Have you ever dreamed or starting a business only to remember how expensive it is? Starting a new business is an exciting prospect, but it is also an expensive one. Some people have the capital set aside to start up their new franchise or business, but many are dependent on loans to fund their venture.

The Small Business Administration (SBA) is a cabinet-level federal agency dedicated to the support of small businesses. Among other forms of assistance and training the SBA helps small businesses to get off the ground by providing multiple SBA backed loans for various purposes. The SBA does not directly loan out money, but provides a guarantee between the business owner and loan provider. Many lenders are wary to loan money to business owners who do not yet have much cash flow and credit, or sufficient collateral and experience. When loans go through the SBA however, their support reduces the lender’s risk of losing money if the business owner is unable to pay their loan back. Additionally the SBA professes to provide “lower down payments, flexible overhead requirements, and no collateral needed for some loans,” making them a safer option for someone looking to start a business.

SBA loans do have minimum requirements that applicants must meet. Points such as what your company does, who you are as an owner, and your company location. You must be a for profit company that operates legally and is registered with the SBA, conduct business within a physical location in the US or its territories, place some investment of your own into the business whether time or capital, and be unable to take loans from another financial lender. There are a number of different SBA loans, including 7(a) loans, 504 loans, express loans, and microloans.

7 (a) Loans

7 (a) Loans

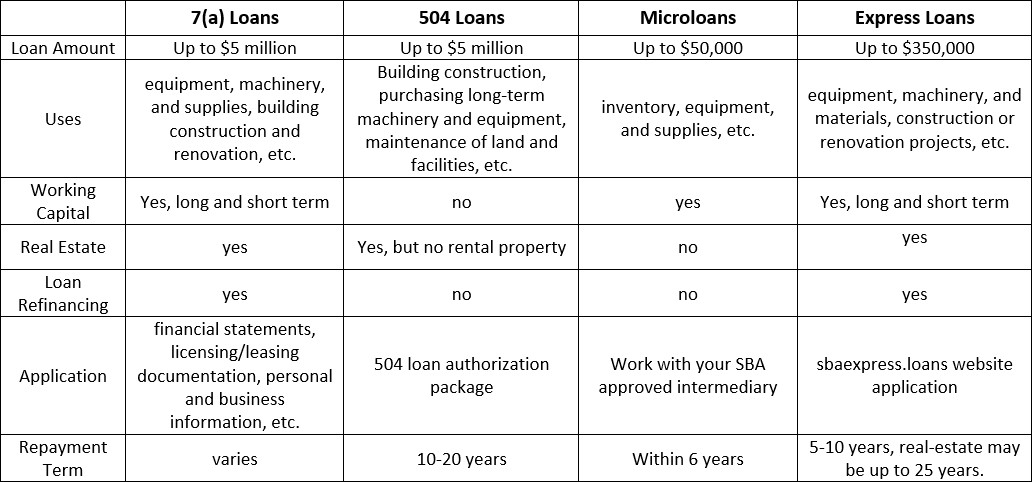

The most common loan from the SBA is the 7(a) loan that allows up to $5 million to small businesses needing working capital, refinancing for business debt, and large scale purchases. It is the best option for business expenses involving real estate. A 7(a) loan can be used for long and short term working capital, equipment, machinery and supplies, real estate purchases, building construction and renovation, starting or acquiring a business, expanding a business, and in some cases refinancing business debts. The ability to use SBA loaned funds for practically any real estate purchases is unique to the 7(a) loan option, as the 504 loan prohibits the use of loaned money for rental properties, and microloans prohibit the use of loaned money for real estate property.

To apply for these loans you need a number of documents including financial statements, previous loan information, licensing and leasing documentation, and information about yourself and your business. The list of exact eligibility requirements and required application documents can be found on the SBA website on the 7(a) loans page. To pay back a 7(a) loan you follow the same process as you would with most other loans paying principal and interest monthly. Additionally there is no prepayment penalty for loans that mature in less than 15 years.

504 Loans

504 loans are geared toward growing businesses and creating job opportunities with long-term fixed rate loans of up to $5 million. According to the SBA, these loans are meant to finance the construction or purchase of new or existing buildings and long-term machinery and equipment or the maintenance of land and facilities. Unlike 7(a) loans these cannot finance working capital or previous debt. Additionally 504 loans are not to be used for uncertain ventures or investment in rental property, making them less effective for someone hoping to enter the property management industry.

The 504 loan eligibility requirements and application are somewhat different from those of other loan options. The SBA states that to be eligible for a 504 loan you must “Have a tangible net worth of less than $15 million and have an average net income of less than $5 million after federal income taxes for the two years preceding your application.” These loans are only financed through SBA certified and regulated Certified Development Companies (CDCs). Additionally this loan application requires a 504 loan authorization package that can be found on the SBA site as a link on the 504 loan page. The repayment of these loans takes place over a longer period of 10 to 20 years with varying interest.

Express Loans

Express Loans

SBA Express Loans are similar to SBA 7(a) loans, however they are not directly through the SBA but rather through https://www.sbaexpress.loans/. These express loans provide a fast turnaround time for potential borrowers with approval or denial received within 36 hours, and funds, if approved, within 90 days. All the other forms of SBA loans take significantly longer. Additionally, unlike 7(a) loans, express loans only provide business owners with up to $350,000. This is plenty for many small businesses such as an All County® property management franchise, however for larger business startups it may not provide enough. In those cases the 7(a) loan would be the better move with its higher limit and similar uses. Like a 7(a) loan, express loans can be used for long or short term working capital as well as for purchasing real estate, equipment, machinery, and materials, construction or renovation projects, establishing, acquiring, or expanding a business, and refinancing existing business debt. The repayment terms for an Express Loan are similar to those of the 7(a) loan as well, with a 5-10 year payment period except for in the case of real-estate which may be up to 25 years. No collateral is required for loans under $25,000.

Microloans

Microloans are, as the name implies, smaller loans up to $50,000 given to assist in the creation and expansion of small businesses. They can be used for most purposes to fix or improve your business including working capital, inventory, equipment, and supplies. Real estate and the payment of existing debts are the two uses barred by microloan rules. To apply for a microloan you will work more closely with your SBA approved intermediary to get loans from specific nonprofit or community based organizations. A form of collateral and the personal guarantee of the business owner may be required for these types of loans. The repayment of a microloan must be complete within 6 years, however the terms and interest rates of the loan repayment will vary by circumstance.

SBA Loans Summary

SBA Loans in Practice

SBA Loans in Practice

Many All County® franchisees have utilized SBA loans to get their property management businesses up and running smoothly. They use the money for startup costs including their lease, equipment, technology, and supplies, signs and marketing, various professional fees and deposits, and whatever other charges happen to come up within the early stages of business operation.

Conclusion

There are many forms of funding available for those who wish to start their own small business. With help from the SBA you can use 7(a), 504, or microloans to build the business of your dreams. Here at All County® we encourage the use of SBA loans if you do not have access to the capital needed to fund your new franchise, because we know that they can help you get off the ground and build a property management franchise you can be proud of.

Sources

https://www.sba.gov/funding-programs/loans

https://www.forafinancial.com/blog/working-capital/sba-loans-franchise-business/

https://www.sba.gov/funding-programs/loans/7a-loans

https://www.sbaexpress.loans/sba-express-glossary/2017/5/12/what-is-an-sba-7-a-loan